Are We In For A Crude Awakening?

How to profit from the panic in this inaugural edition of ROI monthly.

Month In Review - September:

All eyes were on Fed chair Jerome Powell this week and, as expected, he announced the decision to raise the FFR by 75 Basis Points.

As a result, equity and commodity markets were thrown into a panic as a result with oil, the most traded commodity in the world, down 12.28% mom while gold dropped 5.3% on the back of rising real yields.

Monthly:

Note: the staggering 21.97% increase in the US 10 yr note yield (TNX) MOM!

This is traditionally the most important instrument used by investors globally to ‘discount’ expected returns from other asset classes.

For those new to finance, interest rates act like gravity against other assets i.e: when rates rise, asset prices fall (ceteris paribus).

This is why the capital markets hang on every word uttered by the US Fed, as they raise the central banks cash rate (FFR), the cost of borrowing increases for the US government and commercial banks, which leads them to increase the rates they pay/charge on their obligations i.e: the yields bond investors receive on their US 10 year notes and/or the interest retail savers earn on their bank deposits.

Obviously then, if one is getting a higher nominal yield on their bond investment backed by Uncle Sam, one is less inclined to take the risks associated in investing in equities (stocks). As such, the higher the yield on bonds (measured by TNX above), the higher the hurdle rates investors will use when evaluating the expected returns on stock investments.

Whilst in December last year the Fed expected to have raised rates to only 0.9% by Dec 2022, the current FFR stands at 2.33% in one of the sharpest hiking cycles in history.

Two key questions are on my mind:

Given the US Government’s debt levels, how high can they afford to push their cost of borrowing? I.e. at what point will we see the much expected Fed pivot?

Given that rising US rates lead to an influx in capital flows strengthening the US dollar’s strength Vs other currencies (measured by the DXY), at what point does that cause emerging market sovereigns to simply tap out and default on their dollar-denominated debts?

The current central case for where the FFR will be in Dec 2023 stands at a whopping 4.5%!!

If this is true, ‘ we ain’t seen the half of it’ in terms of painful drawdowns in risk assets.

This is because rising FFR pressures the 10 yr yield to rise, or else the Fed needs to artificially suppress the yield on longer dated bonds by printing reserves to buy the bonds (hence lowering yields) in a process known as yield curve control.

Take home message: higher FFR = likely higher 10 yr yield = downward pressure on general stocks.

I’d expect stocks to continue to fall, most heavily in sectors not making any money and with massive multiples (click here to access a trade I’m making to potentially profit from this).

So, with non-yielding assets getting crushed in a higher yielding environment, where am I positioning (hiding) to preserve capital and profit?

Let’s take a look in our Month ahead segment.

October:

I remain long and strong in my conviction that we are merely in a cyclical correction in a secular bull market for energy.

Crude oil is down 12% on the month, yet despite everything thrown its way this year, from rate hikes and recession fears to record SPR release, the price per barrel is still up 7.4% on the year.

Inventories continue to draw (see below) and with the SPR scheduled to end this month, in addition to OPEC+’s reticence/inability to cut production, not to mention sanctions on Russian oil expected to kick in in December, we are in a dangerously tight physical market which could easily see oil prices re-test their previous all-time high of $140/ BB.

The US mid-terms commence the 8th Nov, which may lead to an increase in the tendency for politicians to push for consumer subsidies in exchange for political favor - which does nothing to increase the supply and much to maintain demand, further putting supply pressure on an already tight market.

Oil expert and CIO of Bison Interests, Josh Young, has long suspected that OPEC is reaching the limit of its spare capacity, meaning that the idea that the kingdom of Saudia Arabia can simply and quickly increase output to offset the impact of the SPR release ending is a dangerous fantasy of policy makers.

Oil may continue to chop sideways for now, but given the lack of supply I expect a somewhat stable floor with a strong possibility for a shockingly high upside in prices as the SPR will need to be refilled, right at the time when Russian crude is set to be banned, swinging make-shift supply into more demand.

Ben’s Buys.

What’s Ben Buying This Month?

In this segment I give you my take on a particular stock, including my investment thesis and valuation estimate.

*Disclaimer: I am not a financial advisor and this is NOT financial advice*

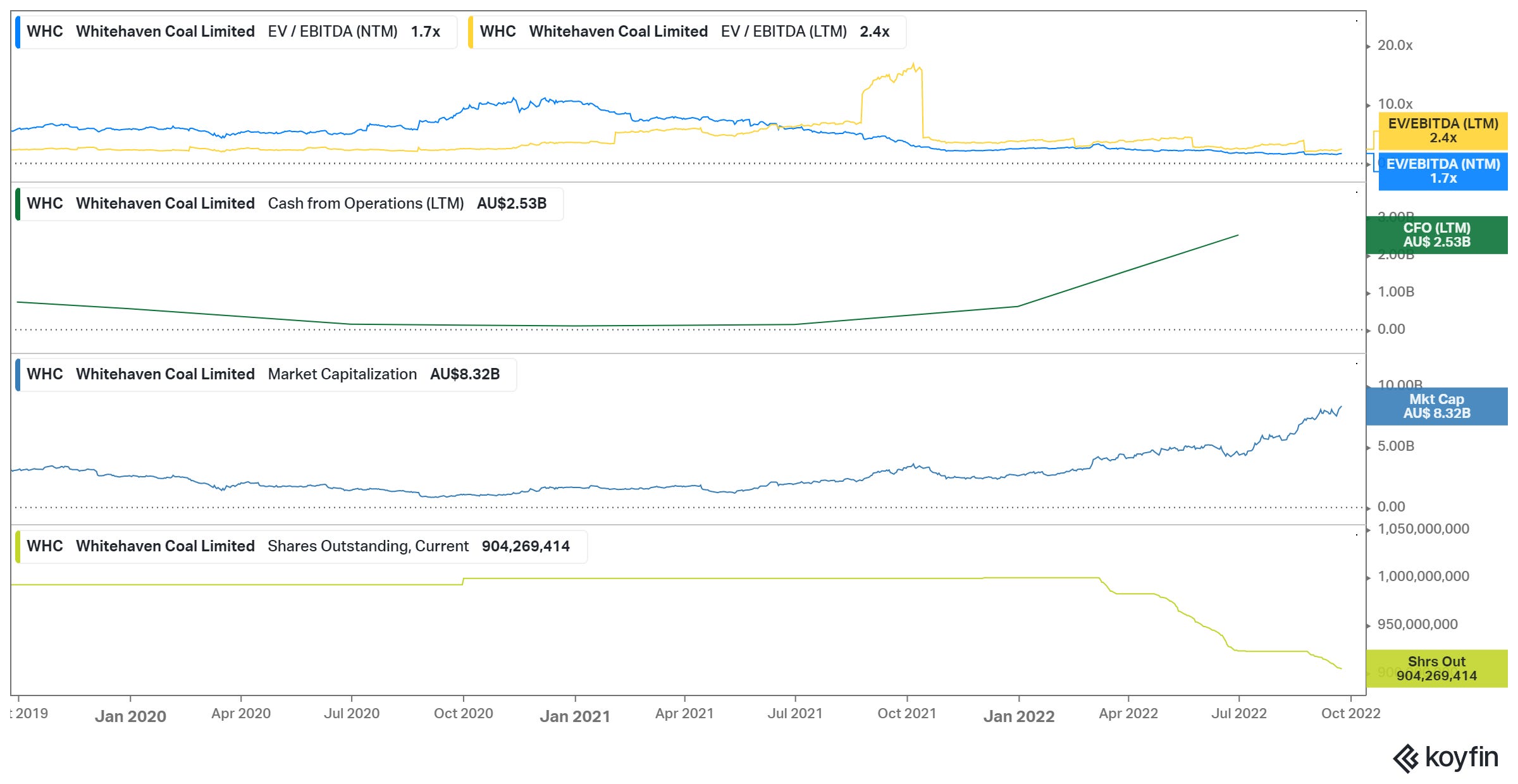

This month’s stock is Whitehaven coal (ASX:WHC), an Aussie coal producer that has been a stellar performer up 227% YTD!

The obvious question then is, well isn’t it too late to buy now?

Answer: I don’t think so.

Here’s Why: Forget the nominal share price, focus on the amount of cash or profit an investment can produce Vs the cost to buy the company. You can measure this by EV/FCF and EV/EBITDA respectively.

Incredibly, if you use this as a measure of value, you can see that you’re actually paying less per unit of profit than you would have 3 years ago. (see below)

Another thing to consider is the balance sheet. WHC is now completely debt free!

Not only that, but they have been buying back shares at a frenetic clip - recently they filed to buy back 25% of the entire share float!!!

As a shareholder, this gives me a greater claim on their future cashflows, as management are effectively buying out my other business partners (other shareholders) with company profits.

With over 20 years left of productive capacity, “ESG” psychosis preventing other capital investment in the sector, and Europe’s failed energy policies leading them to revert back to heavy coal use for electricity generation I think the coal price is set to stay higher for longer.

I see the chance to buy more WHC shares at a FCF yield of >25% with management buying back so much of the float to be an incredible opportunity.

One savvy fund manager I know also thinks so.

Emanuel Datt of Datt Capital, has generated annual returns to his investors of over 22% over the last 3 years.

He shared his thoughts on WHC in this interview here

Analysts estimate WHC to buy back 25% of SOI and produce $3.37 FCF per share in ‘23. As such, I opine that a price of $13.50 is not unreasonable, offering a 25% FCF before considering a much reduced share count.

This edition is free to celebrate the debut of the monthly letter. Let me know what type of content you’d like me to cover moving forwards.

Until next time,

All the best.

Benjamin