Stock Updates: The Problem Children

The 'high torque/high maintenance' cherubs: SBSW

Welcome to the ROI club.

Sometimes I forget I have a rather particular personality and disposition (not for long however as those closest to me always remind me) and, as such, occasionally forget that stock market price volatility induces tachycardia in many whereas I tend to go into a mini coma, opting to sleep my way through to the other side.

Some followers find my relaxing of content-output during these times unnerving and as such I thought I’d open a mini series called ‘The Problem Children’ where we can use price drawdowns as an opportunity to review the thesis and valuations around certain topical companies. These might be companies that I either own, or have owned in the past and may be considering a re-entry point.

Today’s focus is a review on one that’s popular to talk about, yet not so popular to own Sibanye Stillwater (SBSW).

Before digging in, I’d like to reiterate my long term thesis for secularly higher inflation AND volatility remains unchanged and my sentiments with regards to the recent volatility are best summarised by this quote from the great Murray Stahl

"I’d rather volatility than debasement”.

Sibanye Stillwater, SBSW.

Looking at price before doing a valuation represents a flaw in one’s thinking but, given that’s what 99% of people do I’m going to do the same here in order to make myself more relatable (hopefully).

Through options and scaling in in tranches my position is marked down about 10% across my portfolios so not so bad, but enough noise is being made on X for me to revisit my notes in top-down style.

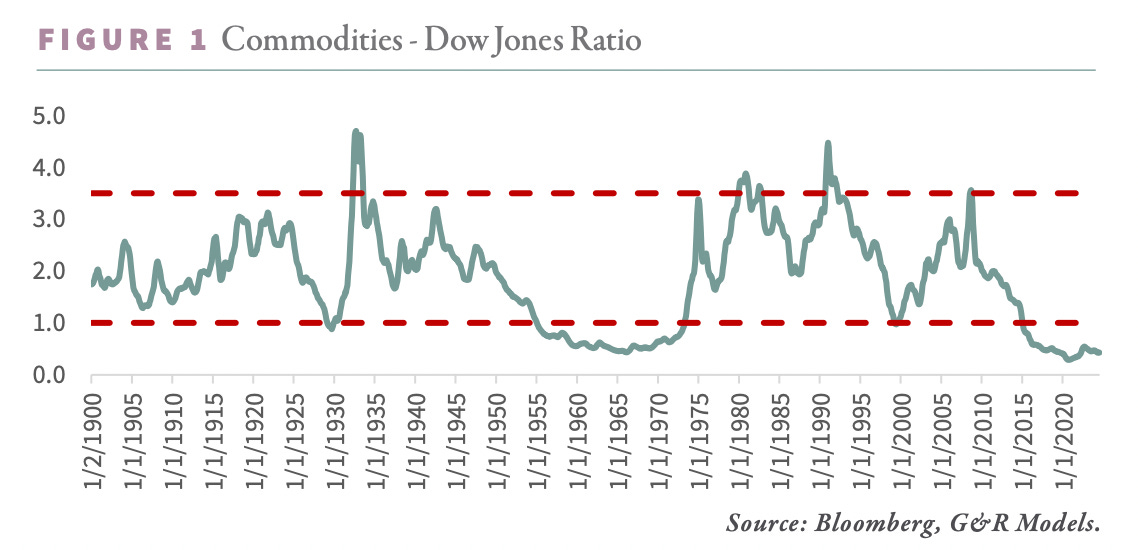

My macro thesis on commodities is well known and hasn’t changed so I won’t repeat it here, however the below chart from Go-Rozen is your reminder as to where we are in this cycle with regards to broad equities V commodities.

On a meso-economic level, palladium/gold has basically never been cheaper.

SBSW sells both commodity metals (PGMS) as well as monetary metals (Gold/silver) so it seems to be in the sweet spot of my commodity-boom, monetary debasement theme.

In my head I visualise my portfolio structured in a “barbell” but rather than the two ends of the bell hedging two different macro outcomes (inflation/deflation beneficiaries), my barbell is purely positioned for a higher inflation outcome over the decade. One end of the bell lies the ‘Capital light/hard asset’ business interest I’ve been covering a lot lately, on the other lies the ‘torquey/deep value’ plays.

SBSW definitely lies at this end of the bell.

So that’s the macro/sector commentary.

On a micro level, during price volatility I always ask myself (non-facetiously) ‘ Why did I buy this originally?’

So here’s the answer in a nutshell:

SBSW holds roughly 70M Gold equivalent ounces (GEO) in reserves. A $2,000 / GEO price implies an undiscounted in-situ reserve value of ~ $140 Billion. Research from Crescat Capital suggests that in a bull market these types of reserves can reach an average acquisition price of 20% of in-situ reserves, implying that SBSW could conceivably reach a valuation of ~$28 Billion.

Obviously this is highly imprecise and will take years to play out (should it play out). My uncle Rick (Rule) is fond of reminding us that most of his 10 baggers took 5 years to play out.

However, $28 Billion as a target valuation is a huge margin of safety given the stock today trades at an Enterprise Value of merely $3.6 Billion and an even lower Market Capitalisation of $2.7 Billion.

So, there’s a strong chance of a 10x here even before contemplating a higher pricing environment for their PGM. Even if I had to wait 10 years for that to occur my IRR would sit above 25%.

The Risks:

The two main risk narratives I see out there basically boil down to:

EVs will replace ICE and hence the need for PGMs for catalytic conversion

South Africa will cease to exist and hence SBSW is worthless.

I think we can safely discount the first, or at least say it’s a long way off and I actually think the recent results in South Africa were a slightly positive turn around. However, I’m obviously not going to sleep soundly at night relying on SA politics to come through in order realise my investment thesis.

So if I write off the SA assets to zero (68% or revenues) obviously that would be bad for SBSW. But don’t forget, in that scenario the world would lose perhaps close to 80% of its PGM deposits.. so we’d have some other issues and the value of SBSW’s USA deposits would moon shot.

Currently, I estimate their USA PGM reserves at roughly $53 Billion using a $2K GEO price. Discounting that to 20% I’m looking at $10.5B which suggests multi bagger potential from the Stillwater and East Boulder mines alone.

Final Thoughts:

The company recently announced a quasi forward-sale agreement of their gold production which they felt wasn’t being fully recognised. It’s estimated this will add $500 million to the balance sheet with more streaming type deals likely to be on the way for 2024. I think it’s a smart play given gold has hit all time highs and this will allow SBSW ample of liquidity to see out the current PGM weakness and absolutely print cash in the event of a more PGM bull market.

Remember, palladium was 3x its current price in Feb 2022 before the Russia/Ukraine conflict. In that environment they reported $1.1 Billion in net income from that year alone..

If you enjoy my work please do me a favour and share the sub stack.

Take Care & DYODD.

Benjamin

Great one!👌👌