The Mirage of Multiples: A Meditation on LB’s Hidden Value

Decoding the Disconnect Between Reported Earnings and Economic Reality

Hello and welcome to the ROI club.

Inevitably any investor who finds themselves in the fortunate situation to be riding a huge winner either asks themselves or is asked by others whether it’s time to “take some profits”.

Possibly the most contentious of my current sizeable positions is that of Land bridge $LB.

The main reason undoubtedly for the conjecture is the perceived valuation.

My aim in this essay is not to persuade, but rather provide my own musing on the current market multiples attached to Land bridge and to see how they might be perceived differently when viewed through an alternative lens.

If you haven’t already read my piece on water, which I believe is currently completely missed by market pundits, the piece below will provide a grounding for some of the ideas featuring in today’s and future pieces.

Land Bridge Musings

The market, in its infinite restlessness, has a peculiar way of distilling complexity into simplicity, often at the cost of truth. Consider LB, a company whose shares, at their peak this year of $84.7, command a fully diluted market cap of $6.23 billion. With projected 2025 revenues of approximately $200 million, I have, somewhat understandably, received many objections to the implied multiple: 31.15 times revenue.

Interestingly, it will be noted that the SP500, with all if its associated risks and concentration in mature tech sectors, also traded on similar multiples, yet the mood amongst the general ‘x-mosphere’ was buoyant until the recent drawdown.

But what if this multiple, so stark and unforgiving, is not a verdict but a mirage—a distortion born of a perspective that sees only the present and ignores the ‘porvenir’, that which is currently unseen but to come?

Let us begin with the essence of LB: its land. LB is the steward of 276,000 surface acres—a vast expanse, each acre a potential source of enduring revenue with an infinite call option on developing the land to higher and better uses.

The critics, fixated on its 31.15x analysts’ expected revenue over-look the revenue per acre and potential increase of that metric. And it is here, I believe, that the true value of LB begins to emerge.

LB owns 276,000 surface acres, a vast resource that generates revenue through land leases, water sales, and power generation.

According to their latest 10-K filing, LB concluded 2024 with revenues of $110 million, a 54% yoy increase which consisted of resource sales, oil and gas royalties and surface use revenues - which includes produced water royalties and an $8 million deposit for a data centre lease. This is of significance looking forward.

My estimates have LB’s 2025 revenue coming in around $200 million or $724 / acre, whilst management have guided a target of $300 million + by 2026-7, which is just over $1,000 per acre.

At time of writing the market cap is approx $4.62 B, leaving the company priced at $16,739 / acre.

Through this lens, the multiple is seen as 16.7-23x against revenues on a per acre basis, depending on your preference for revenues estimates.

If nothing extraordinary were expected, again this would hardly be considered a bargain.

However, a yield/acre of 4.3% ($16,739/$724) is in line with that of a US treasury, which is unlikely to benefit from inflation whereas land generally does.

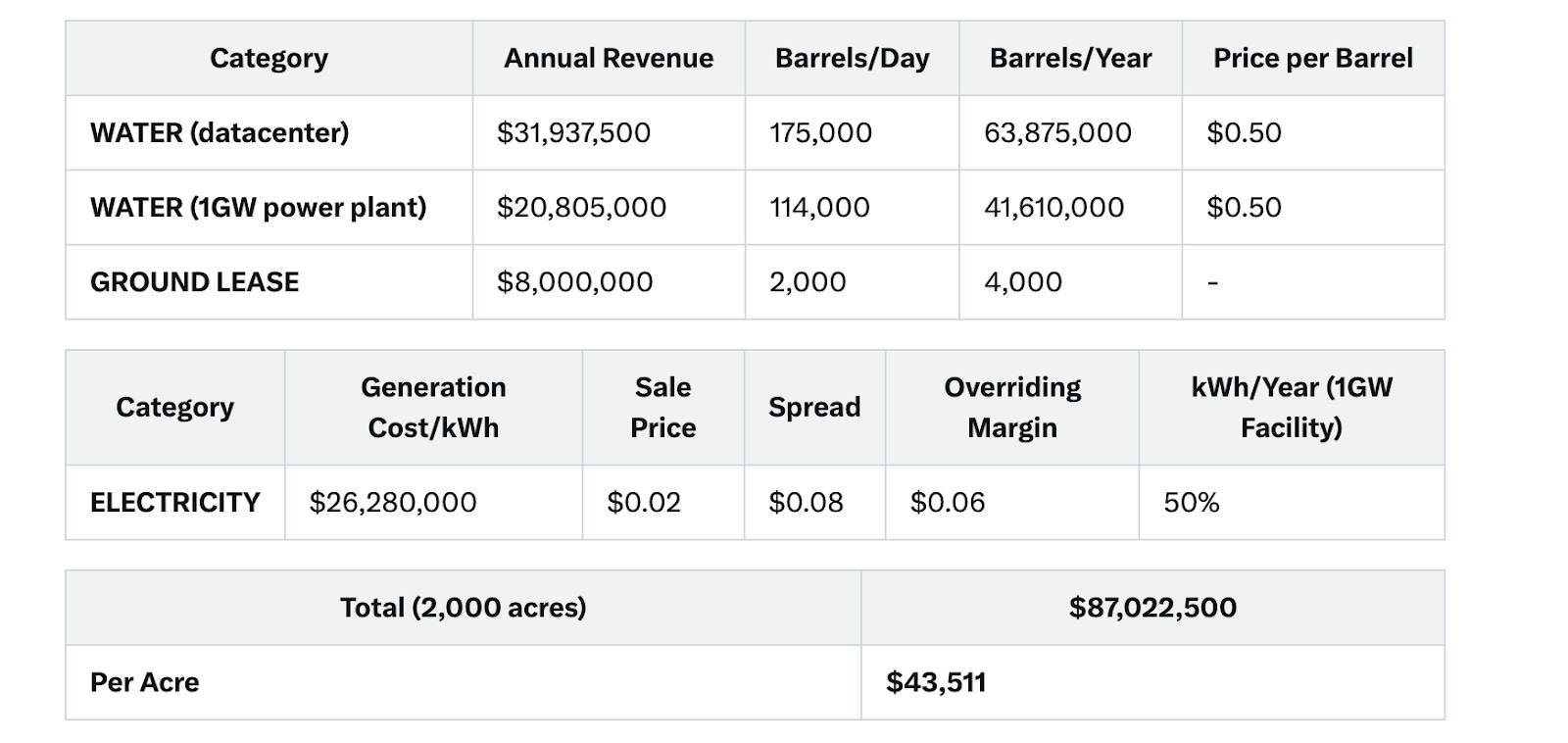

In any case, this figure completely misses something - the earnings that are to come with the first data centre lease signed.

LB’s 10 Q outlines its concept and projections for Its first data center, spanning 2,000 acres and providing an anticipated annual revenue of $87,022,500.

A few remarks on this:

Note the power of the added value to the land, acquired for ~$1,000 / acre, link to prev article

The hidden value here, as I’ve been saying all along, is the water. Handling fees in the permian are currently $0.50-$1.50 / barrel which is only increasing over time. It doesn’t take much to realise the exponential potential this arm of the business has with the water fees alone simply compounding at the historic rate and there’s really no alternative- the produced water from fracked wells must be disposed of correctly and LB via their private sister-company Water-bridge are in pole position to capitalise here.

In the fullness of time a doubling or tripling of revenue from this aspect alone is not out of the question and minimal capital expenditure will be required on Lb’s behalf in order to realise that.

LB management have stated that they currently have 6 sites appropriate for this type of data centre set-up.

$16,739 priced against $43,511 would imply a price/revenue per acre of 0.38x.. and before you throw your screen against the wall, I know that’s only valuing 2,000 of LB’s 276,000 acres… this is merely a musing, remember?

What might this all mean when the concepts of yield per acre is applied through the lens of the equity yield curve?

Analysts estimate the growth of revenues at 78% and then 15%+ each year for the following 2 years.

If the implied yield compresses back to 4.33% by 2028 - assuming projected revenue of $471 million is realised- the implied market capitalisation of LB would be approximately $11 billion.

135% upside from the current market cap of ~$4.62 billion may eventuate with the yield simply remaining on a par with today’s - likely to the shock of all those viewing through the spreadsheet lens of Price/NTM earnings and the like.

In the fullness of time we shall see, it will be fascinating to watch it play out.

Quick reminder grab your ticket to the Rule symposium here

Take care and do your own due diligence.

Benjamin.

PS: please share if you enjoy

Interesting. I might take a small position here when I get some cash again. Ounces and acres.