The Next Franco-Nevada?

Small Cap Royalty trading at half its NAV with multi-bagger potential.

Disclaimer: This article is for informational purposes only and should not be considered as financial advice. Always consult with a professional financial advisor before making any investment decisions.

Welcome to the ROI Club.

It’s not often I make big bold comparisons such as what you’ve read in the headline.

However today I’m making an exception as I think this is probably one of my best asymmetric ideas for those who have the ability to see a business model which can compound at superior rates of return and the patience to allow that to happen over a periods of years.

All the while presented with an opportunity to buy its equity before anyone really knows about it at a valuation of 0.3x book value.

So stick around and please, hit the share button if you took the time to read.

You all know my macro outlook for the future revolves around all but assured higher and more volatile inflation. So why not just buy physical gold?

So whilst physical gold protects against inflation, business models with direct interests in the metal yet without exposure to the cost of producing said metal can actually benefit from inflation disproportionately.

Investment Idea: Gold Royalty Corp (GROY).

We’re going to take a look at how it compares to the company which my uncle Rick Rule describes as the best operating model he’s ever seen in FNV when it was at a similar stage of development and then premium members will get my take on what type of returns I think this company can deliver.

Comparisons with the Industry Leader:

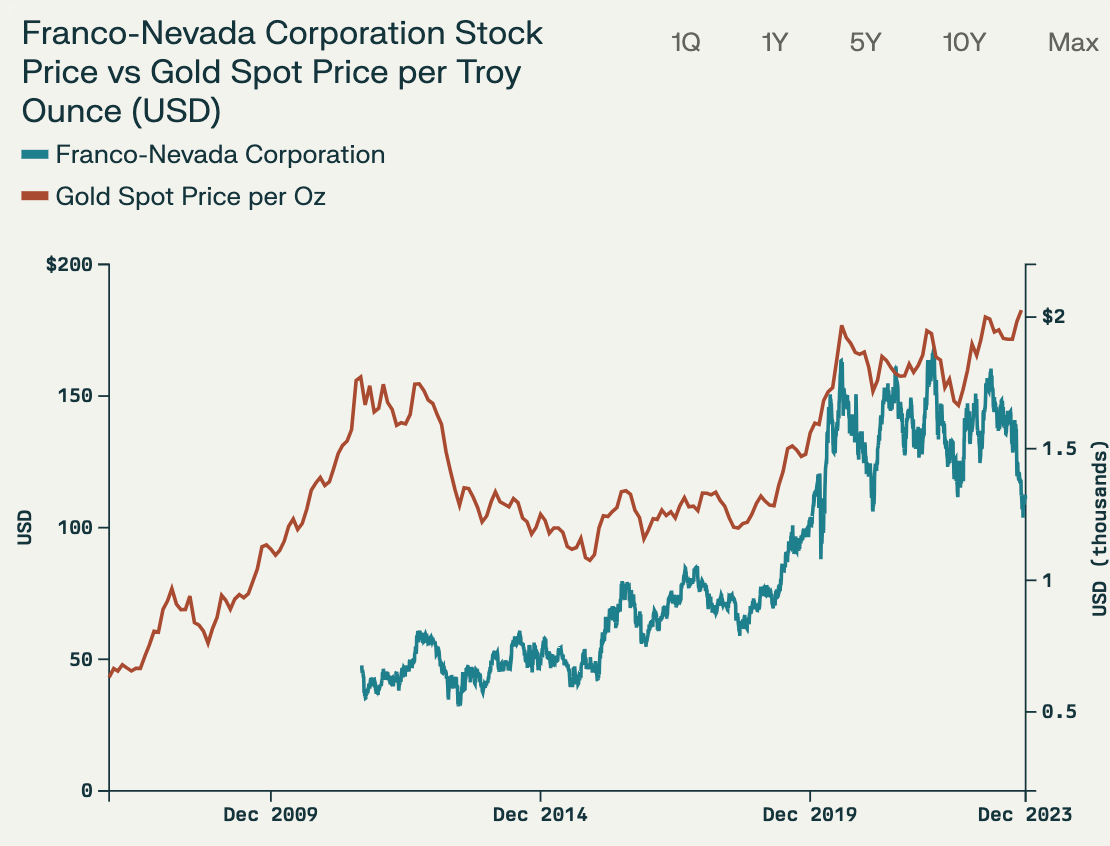

Franco-Nevada (FNV)

Founded in 1983 by Pierre Lassonde and Seymour Schulich, Franco-Nevada started as a small gold royalty company. It was one of the pioneers in the royalty model, focusing initially on acquiring royalties on gold properties in North America. FNV’s early success came from its royalty on the Goldstrike mine, which became one of the most prolific gold mines in the world.

You might say they struck gold. Then found something better, gold royalties.

Gold Royalty Corp (GROY) on the other hand was founded in 2020 by David Garofalo. It was formed with the specific intent of creating a portfolio of gold-focused royalties.

Whilst FNV had to build from scratch and rely on Goldstrike’s cashflows to fund their growth which is slower, GROY is focused on rapidly scaling its portfolio through acquisitions and partnerships. Given the maturity of the royalty sector today, GROY has been able to leverage a more developed market and greater access to capital compared to what FNV had in its early years. However, it must be said that this also means GROY faces more competition.

In 2007 with a market cap (MC) of $1.2 Billion ($1.8B Present Val), FNV held 191 royalty contracts in its portfolio Vs GROY’s 242 contracts at a MC of $224 Million, albeit most are yet to hit production. A rough estimate of FNV’s revenue per contract currently sits at ~$3 million PA / contract so do the math on GROY’s assets and one can imagine a future where the company earns its current market cap in revenue annually…

Comparison Summary:

At a similar market cap stage, Franco-Nevada’s portfolio was more concentrated, with a few high-quality, production-stage royalties that generated significant cash flow and drove the company’s early growth. In contrast, Gold Royalty Corp’s portfolio is more diversified across a larger number of assets and different stages of development.

Yet GROY stock is on offer for circa 0.3x book value, <0.5x NAV, <15x 2025 free cashflow whilst growing revenues at 100%+ YOY with a massive call option on over 198 exploration projects…

If you’re enjoying this, then I invite you to join the ROI club where you get full access to my research and what I’m doing with my investment portfolio and much more.

See you on the other side for a full valuation of GROY.

Keep reading with a 7-day free trial

Subscribe to The Royalty King to keep reading this post and get 7 days of free access to the full post archives.